The Economics of SkillsAn Analysis of Global Tech Talent

Introduction

HR teams are struggling more than ever to adapt to the rapid digital transformation of this era. Key factors like wage inflation, AI acceleration, decentralization of talent hubs, and a “silent reprising” of global labor are colliding, forming a new reality for organizations. In this reality, organizational competitiveness will depend less on labor cost arbitrage and more on the strategic orchestration of skills, systems, and augmented capacity.

Our BrainDesk team dove into tech talent research, analyzing how talent growth is shifting from concentrated hubs in the Global North to a more distributed ecosystem across the South and East. With AI compressing the half-life of technical skills to under two years, tech is reorganizing globally into a network of Builders, Orchestrators, and Synthesizers.

For talent leaders, it is clear. They must evolve their talent metrics from traditional FTE counts to Effective Digital Capacity (EDC)—a metric that accurately reflects how well their workforce can leverage current and emerging technologies to maximize the combined throughput of human and AI systems.

KEY DATA

- By 2027, 40% of today’s core tech skills will be partially obsolete, not due to job loss, but due to skill fusion and AI-enabled workflows.

- Traditional labor-cost arbitrage—that once underpinned global delivery models—has narrowed to below 20%, fundamentally altering how organizations allocate work and capital.

The Polycentric Tech WorkforceGlobal Hubs and Decentralized Talent

Global Talent AcquisitionAdopt a hub + spoke + satellite design

Hubs (U.S., India, China): Scale & depth

Growth markets (Vietnam, Poland, Indonesia): Expansion buffer

Innovation nodes (Israel, Singapore, ANZ): Niche capabilities

THE NEW SCALE ENGINES

APAC & LATAM

Rapid shifts in global talent supply are leading to emerging regions becoming critical engines of growth. APAC and LATAM are experiencing the fastest expansion in tech talent—driven by large, maturing labor pools and consistently rising demand—while

Europe and MEA show steady but differentiated growth patterns as their ecosystems evolve.

The graph below highlights not only the absolute supply numbers across these markets but also the widening talent demand percentages and year-over-year growth rates. It clearly shows where competition for skills is intensifying and where

enterprises may find scalable, future-ready talent pipelines.

Talent Metrics of Supply, Demand, Growth Rate of Global Emerging locations

Note: Talent Growth Rate is depicted as the CAGR of the Talent year-on-year from Nov 2022 to Oct 2025. Talent Demand% is the Job Postings in the last year to the Total Talent Supply.

THE NEXT COMPETITIVE BATTLEGROUNDS

TIER-2 CITIES

Emerging Tier-2 cities across the globe are rapidly gaining prominence as competitive alternatives to established tech hubs. They are experiencing accelerated tech company growth, major hyperscaler and enterprise investments, and increasing R&D activity.

The map below shows locations that have been selected to portray an illustration of Tier 2 cities with rising prominence.

Rising Hubs: Emerging near Tier 1 (or advanced Tier 2) locations

Advantages of Tier 2 CitiesKey factors driving their appeal

Local Duty and Tax Exemptions

Single Window Regulatory Clearances

Relaxation of SEZ Regulations

Attractive Commercial Propositions

Connectivity and Infrastructure

Lower Operational Costs

The Widening Skill GapAnd New Tech Talent Archetypes

JOB FUNCTION FROM 2025 & 2028 (PREDICTED)

Talent Supply & Demand

Software development, cybersecurity, data analytics, and AI/ML roles already face the largest talent supply-demand gaps in 2025. Cybersecurity is emerging as the most constrained function due to accelerating threat complexity and regulatory pressures.

In the graph below, we can see that while most functions show a gradual narrowing of that gap by 2028, cybersecurity sharply diverges. This imbalance is further projected to widen as demand outpaces talent development.

Tech Talent Supply & Demand by Job Function – 2025 & 2028 (Predicted)

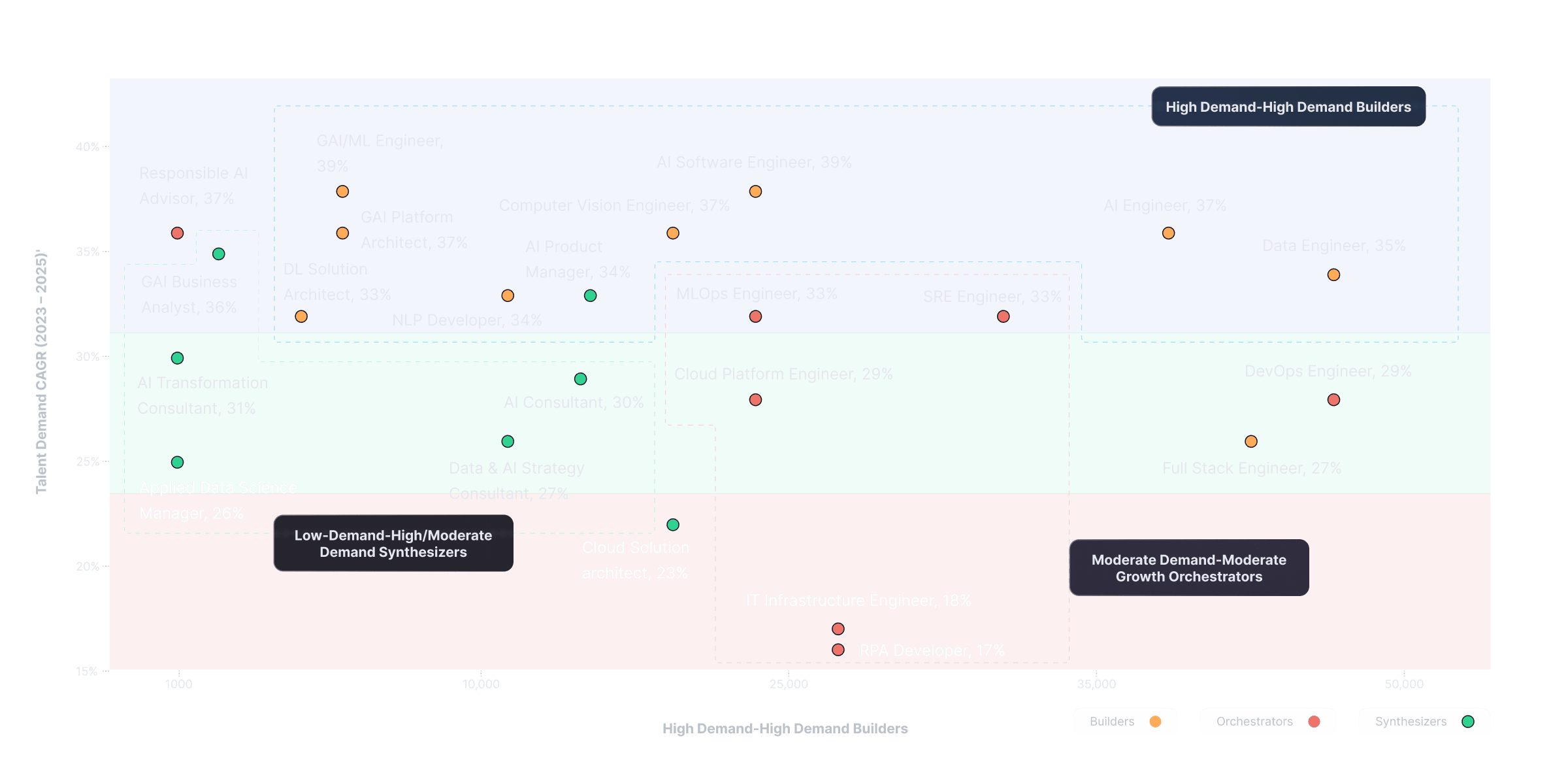

Three ArchetypesOf the global tech workforce

Builders: engineers who create, train, and architect systems

Orchestrators: roles managing integration, deployment, and automation

Synthesizers: hybrid roles bridging business, tech, and AI-enabled decisioning

ONE URGENT SHIFT TO BUILDERS

THREE NEW ROLES

These roles didn't exist at scale five years ago. SWP must recalibrate to hire the right mix of talent, signaling an urgent shift from traditional roles to demand for Builders. The role of HR evolves from filling traditional jobs to engineering workforce composition.

Demand Trends – Talent Demand v/s Demand CAGR (2023-2025)

AI and Skills ObsolescenceThe Two-Year Technical Skill Half-Life

The half-life of tech skills is now less than 2 years, and by 2027, 40% of current tech skills will be partially obsolete due to technical skill fusion + adoption of AI skills.

The graphs below show how the demand for different skills has fundamentally shifted over the past decade.

Talent Skill Cluster Growth Rate: Software Engineering

Talent Skill Cluster Growth Rate: DevOps Principles

Talent Skill Cluster Growth Rate: Testing & QA

Note: * denotes Skill’s Demand Growth Rate % represents the YoY change of the presence of the skill in the Job Postings.

The Age of Augmentation Employees and Human-Machine Collaboration

The next decade of workforce transformation and value creation completely depends on how AI-driven productivity and revenue gains will offset large-scale job displacement. Job creation and automation are converging to drive the future of enterprise value. AI evolution is reshaping work composition, reducing human-only tasks while rapidly expanding AI-led and collaborative human–machine roles across engineering functions.

The graph on the left shows us that AI-driven productivity and revenue gains will offset large-scale job displacement. The graph on the right shows that the share of tasks executed primarily by technology is predicted to grow from 22% in 2025 to 34% by 2030, marking a 50% increase in automation-driven work within five years.

Balancing Job Creation and Displacement

in the Decade Ahead (2025-2030)

Human–Machine Collaboration Becomes

the Dominant Work Model

Why Arbitrage is Below 20%Global Labor Market's Silent Repricing

Four Main DriversReducing traditional offshoring arbitrage to

below 20%

Wage Growth in Emerging Markets

Sustained double-digit salary growth in India, Mexico, and the Philippines is narrowing the cost gap with developed markets.

Globally Competitive Talent Landscape

High global demand for niche roles is forcing organizations to pay a premium regardless of the talent's geographic location.

Proliferation of Remote Work

Remote work has enabled cross-border talent access, but this, in turn, has also triggered pay normalization across markets due to broader competition.

Advances in Gen AI and Automation

Automation is optimizing internal cost structures, making labor arbitrage less central to operational efficiency strategies.

Labor cost can no longer be the primary lever of SWP. Capability, speed, and ecosystem advantages will take precedence. The graphs below shows narrowing cost gaps across multiple countries for the roles of cybersecurity architects and firmware engineers.

Reducing Cost Advantage against USA: Cyber Security Architect

Reducing Cost Advantage against USA: Firmware Engineer

Enterprises Are Paying MoreFor Innovation-Centric Capabilities

Rising Demand for New-Age SkillsFour drivers behind talent premiums

Supply-Demand Imbalance

Early adopters in emerging technologies command a premium until the talent supply catches up.

Accelerated Time-to-Productivity

Candidates with niche skills are reducing ramp-up time by delivering faster results.

Certification or Ecosystem Lock-In

Certified experts in proprietary systems (like SAP HANA, AWS SageMaker) are more expensive to replace.

Direct business impact

Niche skills often directly influence topline growth (like AI/ML product features) or bottom-line savings (like automation via cloud scripting).

Compensation design must continue shifting from role-based pay to skill-based compensation architectures, especially in domains like AI, ML, cloud, and cybersecurity.

Skill Based Pay Premium by Roles

Note: Base Pay reported is for the United States.

Startup vs. Big TechDifferentiated AI Talent Acquisition Strategies

Startups and Big Tech globally are hiring for AI in very differentiated patterns. Startups are prioritizing versatile AI engineers who accelerate GenAI development, whereas Big Tech seeks specialists in frontier models and large-scale AI infrastructure.

Due to this, startups have 35–45% AI skill penetration, i.e., nearly 2 times that of Big Tech. Big Tech, however, commands the largest absolute AI talent pools.

AI Talent Landscape in Tech Startups vs Big Tech Companies

Action Plan for CHROs

Skills expire faster, and AI reshapes work composition as global talent markets further decentralize. Talent leaders must rapidly shift from workforce expansion to workforce engineering.

The future demands a shift from headcount to Effective Digital Capacity, driven by the continuous upskilling of the augmented employee and a strategic, polycentric talent architecture. Ultimately, competitiveness through 2030 will favor organizations that can continuously adapt.

Consider where your workforce is today and what frameworks it must build to stay competitive all the way through 2030.